David Lyman

David Lyman

What Does InsurTechs’ Success Say About the Future of Insurance?

What do incumbent insurers need to fear—or learn—from InsurTech distributors? Investment continues to pour into leading companies such as “unicorn”...

Despite its enormous social and economic significance, the P&C insurance industry continues to face challenges with its reputation and individual insurers struggle with churn. How is so much good work eclipsed by perceptions—and perhaps in some cases the reality—of unfairness? In talking about the industry with members of the general public, you might get the impression that insurance companies were on a par with used car salesmen. Perhaps we should revisit our own prejudices about used car salesmen (and saleswomen), but we might also consider what insurance companies have in common with the bad reputation of that profession and ponder what can be done about it.

The problem with buying a used car is that you’re not sure what value you’re getting for the money. What seems like a fair deal may turn out to be a mistake a short time later. Similarly, many insurance customers may feel cheated if a policy doesn’t cover a loss when they make a claim. In both cases, the customer is at a disadvantage created by an asymmetry of knowledge. The perception is that the car dealer knew what was wrong with the car before the sale—and the insurance company knew that some losses that the customer thought would be covered actually were not. Even when the insurer pays, the loss itself and a lengthy claims process does not leave the insured feeling good.

We have been working with insurance carriers that are using a combination of up-to-date, high quality imagery and powerful analytics technology to improve the transparency of the relationships with their policyholders and agents while mitigating risks before they result in losses.

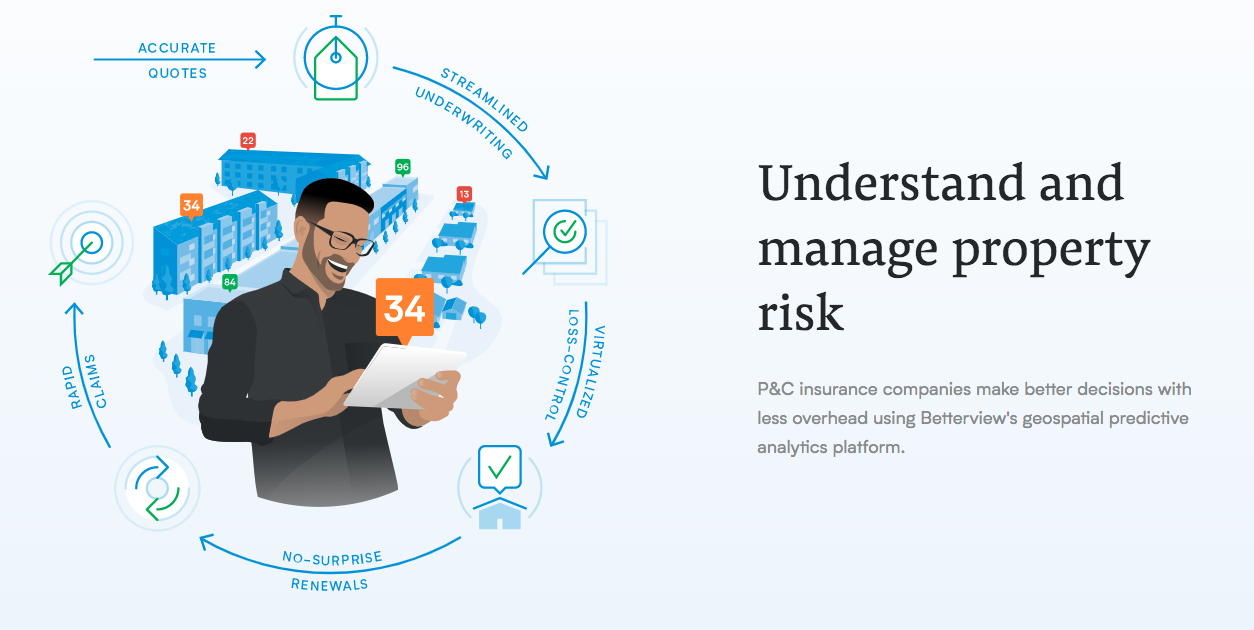

Data, the Great Equalizer

While buying a used car might always feel like a zero-sum game, insurance doesn’t have to feel that way. Just as the Kelley Blue Book and the Internet have reduced information asymmetry to the benefit of consumers, availability of data can benefit insurance customers. As customers gain an understanding of insurance’s value proposition, they will trust their carrier more and be less inclined to switch. Insurers should not look at their data as a competitive advantage over their customers, but as a basis for cooperation with the insured toward the mutual goals of preventing and minimizing losses.

Greater transparency should start during the process of evaluating the property to be insured, and it should take the form of a candid conversation. Insurers should discuss the various aspects of a given property that can make losses more likely, and they should give the customer the opportunity to either agree to exclusions or to mitigate the risk. For example, a swimming pool without a fence adds risk, as does encroaching vegetation in a wildfire zone. A roof in need of repair can increase both the probability and severity of a loss significantly.

By quantifying these risk factors, insurers are able to share an objective, mathematical justification for differences in premium. And to the extent that the risks can be mitigated through efforts on the part of the insured, the carrier and policyholder become partners in risk and loss reduction.

Historically, risk quantification is an easier task for the largest carriers because of their enormous amounts of loss data. That is changing as external sources of data and analysis become available, and as patterns of risk trend away from historical patterns—as in the case of changing storm and wildfire patterns.

Betterview is empowering property insurance carriers to examine properties for specific risk factors which can be discussed with customers at point of sale (quoting), renewal, and time of loss. Betterview’s remote property intelligence platform integrates superior quality data, robust data science and visualization tools. Betterview’s customers are able to make faster, more accurate decisions while strengthening policyholder relationships by providing more transparency into decision making and proactively addressing property risks that have the potential to disrupt the lives and businesses of those policyholders. This focus on transparency and actionability differentiates Betterview from other providers that deliver data.

Trusted Advisor

By involving the insured and agent in a discussion about quantifiable risk factors that are clearly visible in the imagery of the property and how those risk factors affect premium, insurers are transcending the classic indemnification proposition. This change enables insurance carriers to become partners in prevention rather than just payers in the event of a loss. An insurer’s data is no longer a knowledge advantage for the insurer alone, but the basis of an enhanced advisory role. In a paper-based world, the contract/policy is signed, and the parties hope for the best; in a data-driven world, the parties are partners with a dynamic relationship to continually manage risk as it changes over time.

Carriers will gain trust (and retention) from transparently negotiating and renegotiating premium through their new partnership in risk mitigation and loss prevention. They will further enhance their reputation by changing the way they think about the “moment of truth” with the policyholder. Indemnification happens only at the time of claim, but a trusted advisor provides useful information not only when bad things happen, but helps to prevent them, too.

What do incumbent insurers need to fear—or learn—from InsurTech distributors? Investment continues to pour into leading companies such as “unicorn”...

Marcus, a father of four living in a suburb outside of Miami, feels overwhelmed when he is notified of an approaching tropical storm—until his...

Insurers are in the business to pay claims when they happen. Insureds expect insurers to make good on that promise. Historically this has led to a ...