Property & Casualty insurers should be very excited about LiDAR. LiDAR – which stands for Light Detection and Ranging – is a method for remote sensing originally developed to examine the Earth’s atmosphere and map the surface of the moon. Thanks to advances in geospatial technology in recent decades, LiDAR has emerged as a reliable technology with applications across multiple industries.

For P&C insurers, this technology presents a powerful way to identify three-dimensional property features not possible through alternative methods. Insurers who are already leveraging property intelligence, and even those who are not yet doing so, should explore the possibilities of LiDAR in 2023.

What are the Advantages of LiDAR?

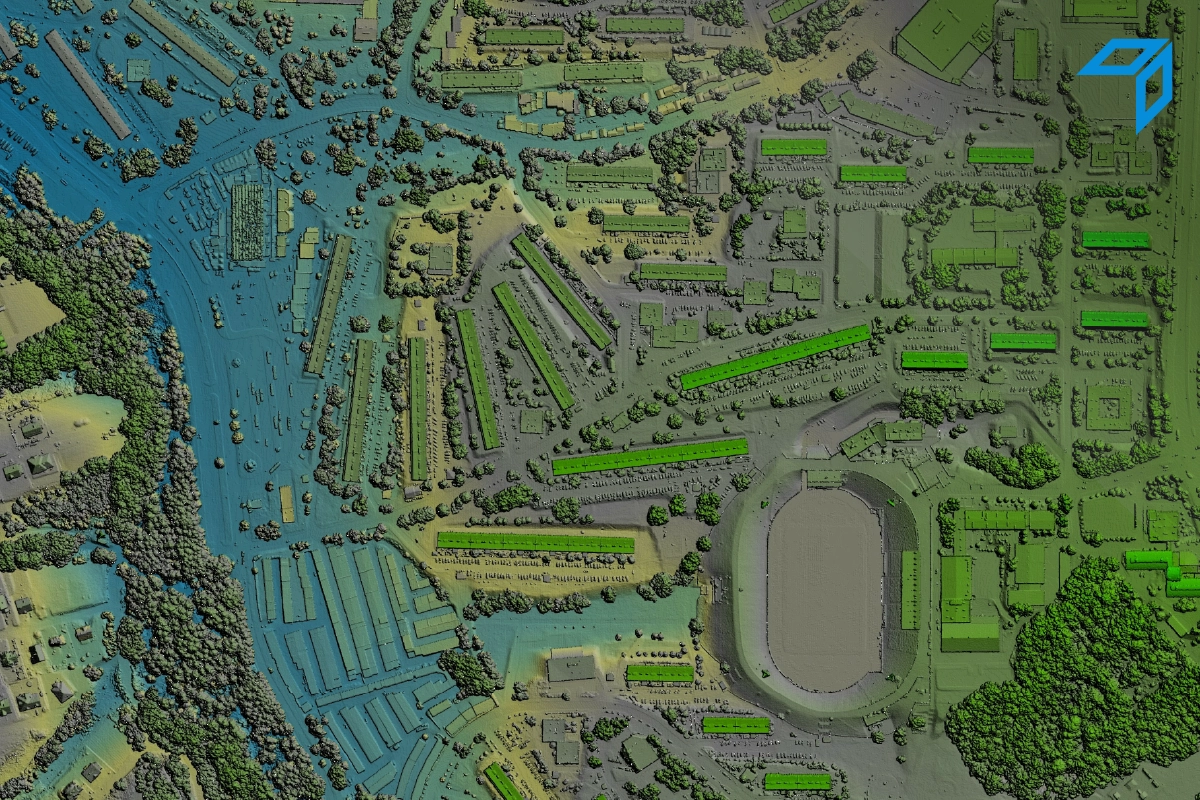

For P&C insurers, the accurate 3-dimensional maps enabled by LiDAR have significant advantages over both on-the-ground inspections and 2-dimensional mapping technologies. Ground inspections can provide a close-up view of real property condition, but they are unsustainable at scale. 2D mapping techniques can cover a wider area than inspections but are unable to detect 3-dimensional attributes such as building height and roof slope. LiDAR solves for both problems, rendering maps that are highly precise while also covering a wider geographic area than previously possible.

How does LiDAR compare to other remote sensing methods like radar? The technologies are similar, but there are crucial differences that allow LiDAR to detect 3-dimensional property features on a more precise, granular level. A LiDAR system primarily consists of a laser, a scanner, and a specialized GPS receiver. For an airborne LiDAR system (static LiDAR is also available), the laser is placed in an airplane or helicopter and a beam is directed at an area on the ground. Based on the amount of time it takes for the beam to reflect back to a sensor, a range is determined. This range is then combined with other geospatial data sources to create a cluster of elevation points known as a point cloud. This is superficially similar to how radar works—the key difference is LiDAR uses much shorter-wavelength light waves, and as a result, returns a considerably more precise point cloud.

Why Insurers Need LiDAR

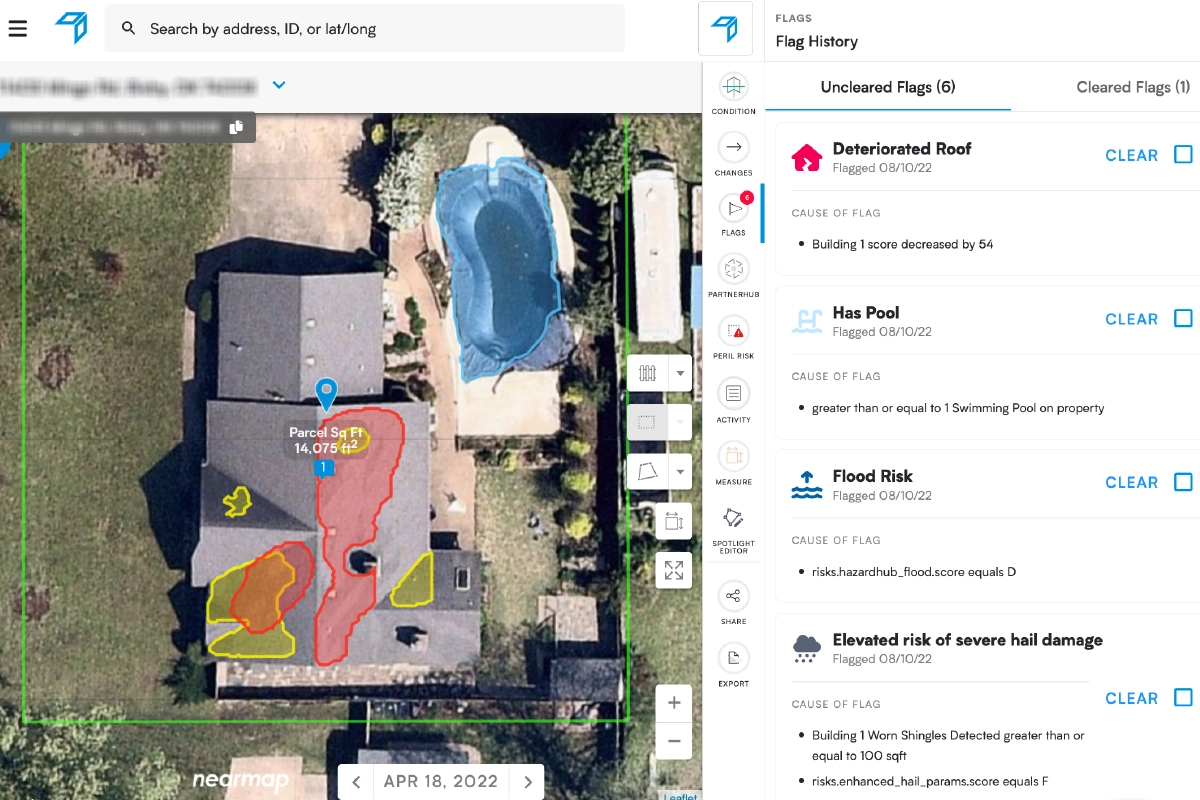

As a method for detecting and measuring 3-dimensional property features, LiDAR is both accurate and reliable. It is particularly useful for detecting roof slope and building height, two attributes that can have a major impact on overall property risk. Determining roof slope is important to determining overall vulnerability, as flatter or stepper roofs have different benefits and drawbacks based on regional hazard. In areas that see heavy snowfall, a steep roof can help prevent the accumulation of precipitation.

On the other hand, in areas that experience high winds, a flatter roof may be necessary to minimize damage. Building height is also relevant for insurers, as higher-story buildings can carry significant liabilities, from high-rise workers sustaining injuries, to more complex fire evacuation plans. LiDAR can also be used to predict treefall, another significant driver of roof damage, allowing insurers and policyholders to work together to mitigate risk before damage occurs.

By using LiDAR in addition to other sources of property intelligence, insurers can improve accuracy and precision at multiple points throughout the policy lifecycle – especially in the detection of 3-dimensional property features. Underwriters can use LiDAR-enhanced imagery to gain a more comprehensive view of property condition, allowing them to properly price risk and avoid premium leakage for both new business and renewals.

LiDAR is still a relatively young tool in the insurance space; the future will no doubt reveal even more ways the technology can help insurers to predict and prevent losses, optimize efficiency, and provide high-quality service to policyholders.

Meadow Green

Meadow Green